With 2019 ended and 2020 beginning, we are writing a series

about markets and the economy. The series is mainly visual, anchored with

charts, but includes brief bullet point explanations of each chart.

Throughout the series, we explore the present bull market

which commenced on March 9, 2009. Our essays to date have addressed the strong

labor market and solid consumer confidence, benign inflation and low interest

rates, unprecedented late cycle government stimulus and what’s been

interesting, even unique, about this bull market.

Today we continue with what’s been interesting about this

bull market before we ultimately analyze what threatens the bull market in 2020

and beyond. To read the previous essays in the series please visit our blog.

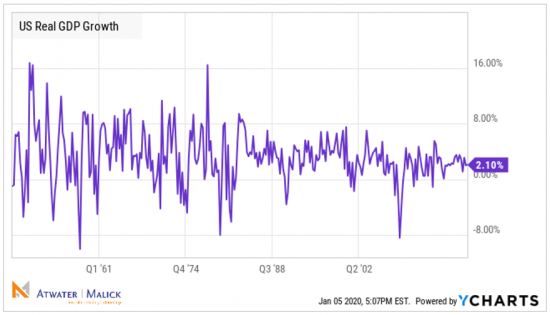

Although the present bull market has offered above-average

returns and duration, it has done so with below-trend gross domestic

product (GDP) growth.

GDP is the most common indicator to

track the overall health of the U.S. economy.

It represents the total dollar value of all goods and services produced

over a specific time period and reflects the size of the economy. The rate of GDP growth, therefore, is the rate

of growth of the economy.

Throughout the present bull market, U.S. GDP has

grown at a below-average rate of about 2% versus the long-term historical

average of about 3%.

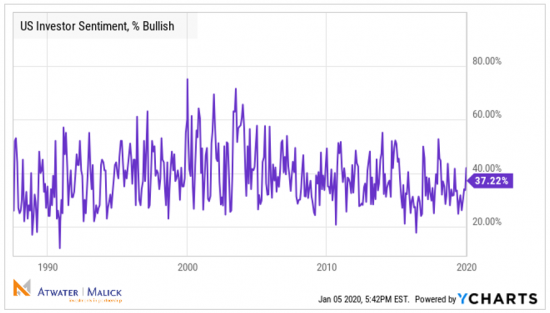

Overconfidence can be

an Achilles’ Heel for bull markets because if investors are too positive it

means that stocks are overbought and vulnerable to a correction or worse.

U.S. Investor Sentiment, Percentage Bullish, is

an indicator that is a part of the American Association of Individual Investors

(AAII) Weekly Sentiment Survey. It indicates the percentage of investors

surveyed that had a bullish outlook on the market. The most extended point of

this bullish survey was in 2000 during the technology boom. This sentiment

indicator reached 75% during that time frame.

The below-average bullish sentiment throughout

this bull market has meant that investors haven’t become overconfident like

they were in 2000. Sentiment is not a foolproof

indicator as sentiment also wasn’t extended ahead of the Financial Crisis. However, all things being equal, it is

healthier for a bull market when it climbs a wall of worry and skepticism

prevails.

Despite below-average economic growth and little

excitement about the stock market, stocks have performed well largely for one

reason – relative value.

The earnings yield on stocks (earnings divided by

price) has far outstripped the yield on the risk-free ten-year U.S. Treasury

bond since 2010.

Primarily as a result of sustained low interest

rates, stocks have offered a better relative proposition than cash or

bonds.

It’s certainly been a bull market with lots of fascinating anomalies. Over the next couple of weeks, our final two notes will examine what might ultimately derail this bull market. We hope your 2020 is off to a great start. Please don’t hesitate to reach out to us as you contemplate your 2020 financial goals.

Intrigued? Get the Full Story.

A collection of financial essays, the Disciplined Contrarian chronicles the most serious financial crisis since the Great Depression — and the second longest bull market in modern history that followed it. Request your free copy today!