As 2019 ends and 2020 kicks off, we are writing a series about markets and the economy. The series is mainly visual, anchored with charts, but includes brief bullet point explanations of each chart.

Throughout the series, we examine the magic of the present bull market. We explore why we are at record levels in the S&P 500 and how we got here. Our first essay talked about the strong labor market and solid consumer confidence, while this essay turns to benign inflation and low interest rates.

Other essays in this series will examine what’s been interesting and even unique about this bull market and, ultimately, what threatens the bull market in 2020 and beyond. To read the previous essays in the series please visit our blog.

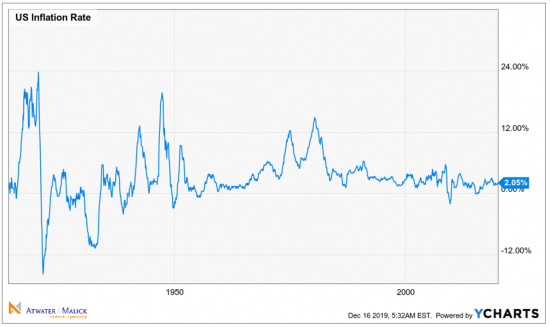

The long-term average U.S. inflation rate is

3.24%, but for this bull market we’ve seen inflation average under 2%.

Since 2012, the U.S. Federal Reserve has

publicly stated an inflation goal of 2%.

Inflation being below average and below target has

allowed the Federal Reserve to institute highly accommodative monetary policy

throughout the bull market.

The adage “don’t fight the Fed” has surely been

true during this bull market. A generous

Fed has led to a docile market.

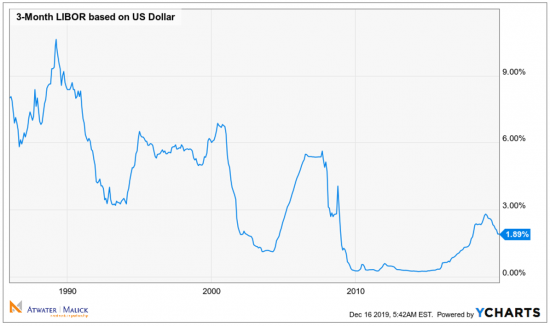

Not only have interest rates and inflation been

low in the U.S., but they have also been low throughout the world.

A low Federal Funds rate (an interest rate the

Federal Reserve directly controls) has much influence over short-term rate

benchmarks like 3-Month LIBOR.

3-Month LIBOR is a benchmark that banks

frequently use to price debt. A low

LIBOR makes borrowing more appealing and as such stimulates the economy. This is surely the case with LIBOR at 1.89%

compared to its long-term historical average of 3.74%.

Low inflation and an active Fed have led to low

longer-term rates as well. The 10-year

presently yields 1.90%, substantially below its long-term average of 6.12%.

The 10-year has a heavy influence over mortgage

rates. Low mortgage rates have kept the

housing market healthy during this bull market.

Most importantly, the 10-year impacts stock

valuations. A low long-term interest

rate theoretically makes stocks more valuable as the discounted present value

of future corporate earnings are worth substantially more at low rates relative

to high rates.

In our next note, we will look in even greater detail at how the bull market could continue into 2020. We hope your holidays are off to a great start!

Intrigued? Get the Full Story.

A collection of financial essays, the Disciplined Contrarian chronicles the most serious financial crisis since the Great Depression — and the second longest bull market in modern history that followed it. Request your free copy today!