As 2019 ends and 2020 kicks off, we are writing a series

about markets and the economy. The series is mainly visual, anchored with

charts, but includes brief bullet point explanations of each chart.

Throughout the series, we examine the current bull

market. We explore why we are at record levels in the S&P 500

and how we got here. Our first essay talked about the strong labor market and

solid consumer confidence, our second turned to benign inflation and low interest

rates, and our third and final essay on “the magic” will focus on the

unprecedented late cycle government stimulus which policymakers accelerated in

2019.

Other essays in this series will examine what’s been

interesting and even unique about this bull market and, ultimately, what

threatens the bull market in 2020 and beyond. To read the previous essays

in the series please visit

our blog.

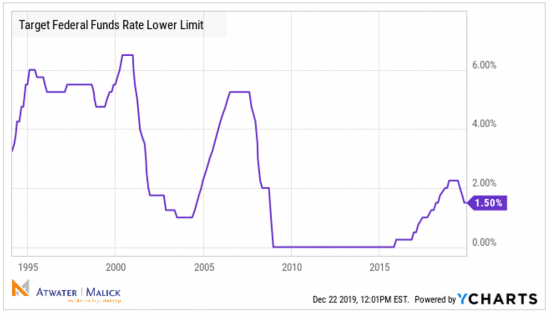

By late 2018, the Fed raised interest rates five

times in an attempt to wane the economy from its aggressive financial crisis-era

stimulus; however, markets began to sour on the strategy and the S&P 500

fell nearly 20% from its 2018 peak to its

Christmas Eve bottom.

The Fed quickly shifted gears in 2019 and has

lowered rates three times this year, spurring a banner year for the S&P 500

following a lackluster 2018.

The Fed Funds Rate stands at 1.50%, well below

its long-term average of 2.58%.

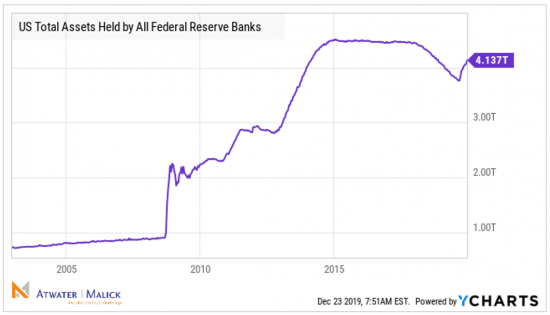

Not only has the Federal Reserve aggressively

lowered interest rates in 2019, but it has also reignited its quantitative

easing program. Quantitative easing is

when the Fed buys bonds (currently Treasury securities) from the open market,

thereby injecting cash into the economy and creating new money.

The Fed’s balance sheet had been contracting

somewhat as the Fed was letting the bonds it owned mature and not reinvesting

the funds.

However, after recent problems in overnight

funding markets, the Fed has once again aggressively begun buying bonds, no

doubt increasing investor risk appetites and helping the market’s 2019

“melt-up.”

The Fed’s balance sheet expansion, which started

as an emergency response to the financial crisis, is beginning to look more

like an economic addiction, much like low interest rates.

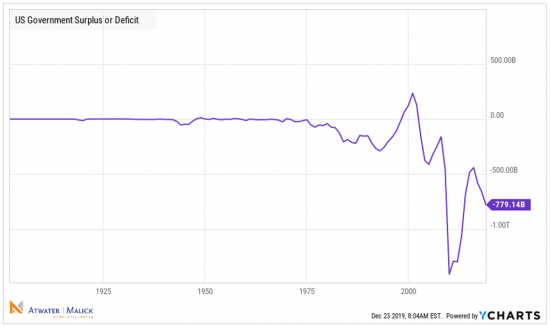

Stimulus is coming not only from the Federal

Reserve in the form of lower interest rates and quantitative easing (monetary),

but also from Congress (fiscal).

At this stage of an economic cycle you’d expect

to see the deficit narrow as it did for several years post-financial crisis, shrinking

to under $500 billion.

But lately we’ve seen an explosion in the annual

deficit with it heading to almost $800 billion.

U.S. stock markets and the broader economy are

benefitting from large corporate and personal tax cuts, while the deficit bears

the brunt.

In 2019 the least talked about and most important aspect of

the bull market has been unprecedented government stimulus. In our next note, we will begin to take a

closer look at what’s been particularly interesting and maybe even unique about

the bull market. As always, thanks for

your support and your referrals. We

truly appreciate working with you.

Intrigued? Get the Full Story.

A collection of financial essays, the Disciplined Contrarian chronicles the most serious financial crisis since the Great Depression — and the second longest bull market in modern history that followed it. Request your free copy today!