What to Expect from the Market

Published On: June 27, 2016

Written by: Ben Atwater and Matt Malick

There is extreme danger in relying on the accuracy of any prediction. The future is much too unknowable to venture guesses on how the economy will grow, what will become of interest rates and inflation or how profitable corporations will be.

That said, with investing we need to make some baseline assumptions about how various securities will perform in order to create retirement income plans for clients. Others in our profession need to make guesses about how endowments will perform to determine how much to distribute to support charitable enterprises or what returns a pension fund needs to achieve in order to pay its retirees.

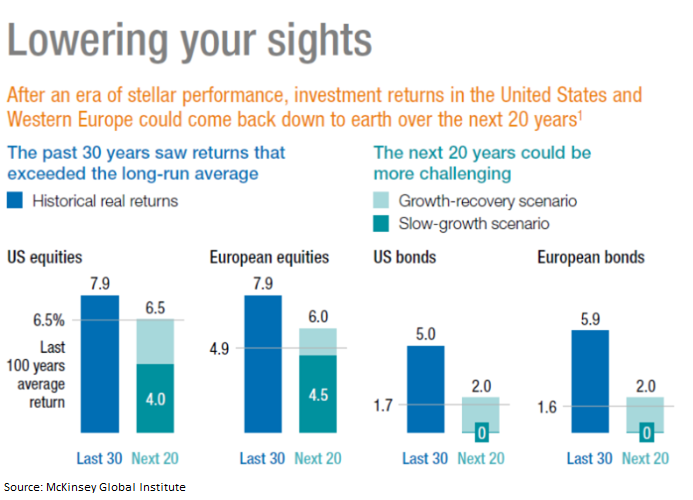

Recently there has been considerable literature about diminishing future investment returns. Much of this stems from four legitimate concerns: 1) a very low interest rate environment which, in and of itself, is indicative of lower forward bond returns; 2) a low rate of inflation; 3) poor economic growth and 4) full equity valuations. The graphic below is from a recent McKinsey Global Institute study that suggests future returns will be significantly lower than the historical average of the last 30 years.

We are somewhat heartened at the continued pessimism about financial markets. As contrarian investors, we believe that skepticism is the perfect environment for the market to produce healthy returns.

Just for fun, let’s accept two of the above headwinds – low interest rates and low inflation, which are linked phenomena – and reject the other two, poor economic growth and full equity valuations. Let’s assume that the economy can get back to trend growth simply on the basis of pent up demand and that equity valuations in a low interest rate world can expand significantly, while technological advancement and globalization keep inflation and interest rates low. This would lead to anything but below average future returns.

Again, there are too many variables to know with any certainty what will happen, but the continued pessimism about investing in general and future returns specifically makes us believe the reality could be different than the expectations. It is fascinating to note that we have not seen a single research piece since we started our firm in 2008 to suggest that future investment returns will be higher than average – nobody thinks such a fantasy is even possible.

Regarding the retirement income planning we do for clients, the implied return on a 65% stock and a 35% bond portfolio (a “balanced” investment approach) that we tested for a client in a “poor” market scenario is 4.76% per year over the next forty-plus years. Our software uses a 2.5% inflation assumption, meaning real returns would be just 2.26% per year. Using McKinsey’s numbers, their “growth-recovery scenario” for U.S. stocks and bonds at a 65% stock and 35% bond allocation is 4.925% over the next twenty years, or 2.525% real returns net of 2.4% inflation. In McKinsey’s “slow-growth scenario,” they show the same portfolio returning 3.3% per year over the next twenty years with 1.6% inflation for a real return of 1.7% – this strikes us as unreasonably low.

Although the current pessimism has a potentially optimistic result, when making projections for clients, we will continue to be cognizant of a “poor market” scenario and do everything we can to prepare clients accordingly. However, we can’t help but be encouraged by the almost unanimous forecasts for lower future returns.

Mar 21, 2024

Feb 27, 2024